The smartest way to manage U.S. sales tax.

We handle calculations, filings, registrations and notice management, across every U.S. jurisdiction. Powered by AI-native infrastructure and proactive expert support.

Trusted by 1,200+ finance and accounting teams.

50+ states & territories. 13,000+ jurisdictions. Zero room for error.

U.S. sales tax is a maze of changing rates, taxability rules, and nexus thresholds. And until now, you only had two options:

Buy software. Do the hard work yourself.

Hire consultants. Pay a premium. Move slowly.

Zamp is the next-gen managed sales tax platform.

Automation at scale, with experts who step in when it matters. We own the outcome, not just the software.

How Zamp fully manages sales tax — from first sale to final remittance.

Built on AI-native infrastructure with expert review where it matters — accurate by default, defensible under audit.

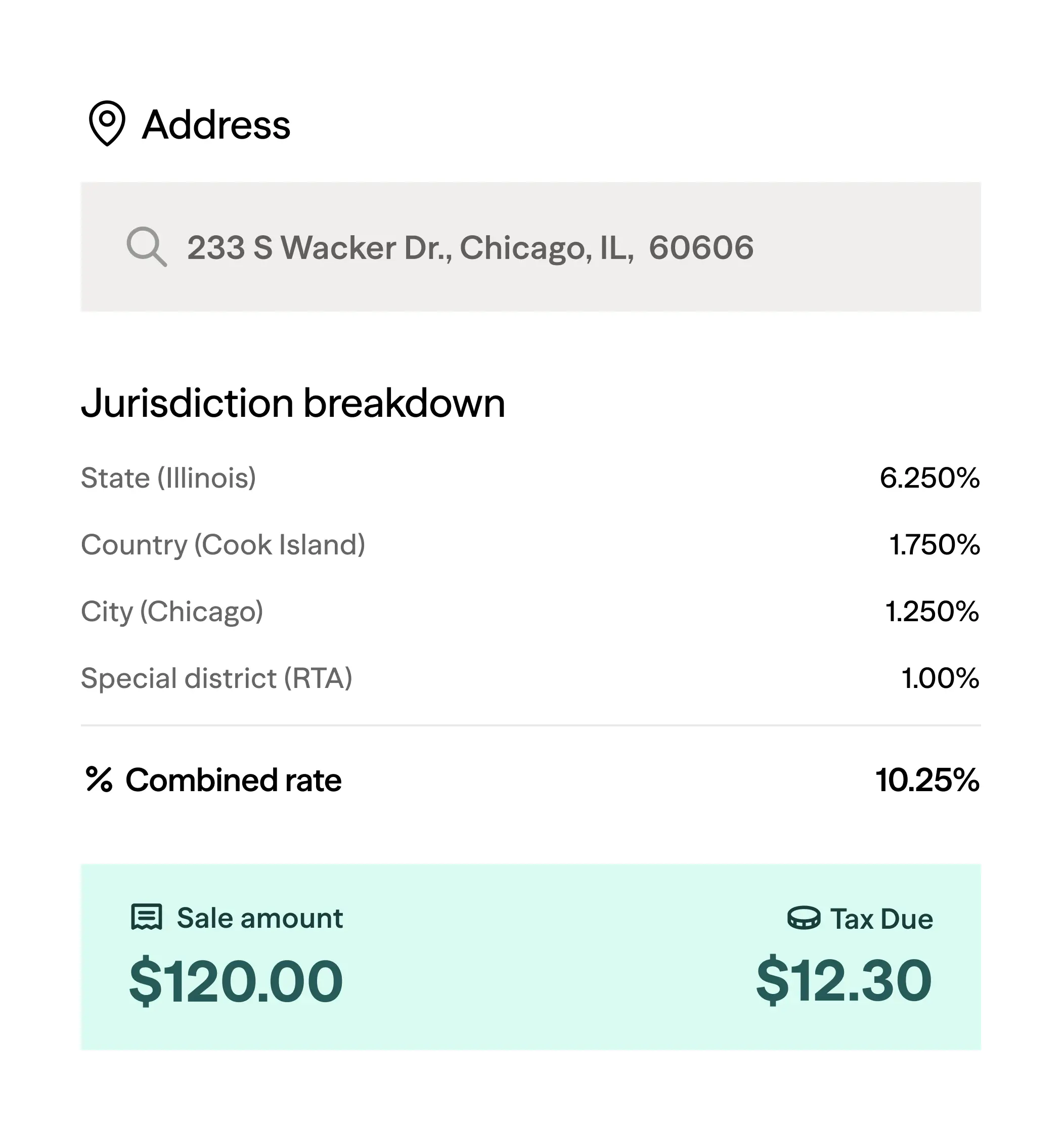

Rooftop-accurate tax calculations.

Our proprietary tax engine uses geospatial data to determine the exact rate and taxability for every sale across all U.S. states and territories — fully audit-defensible.

We validate address data instantly and apply the latest rules to prevent errors before they occur.

We maintain and update our rule library continuously—using AI to deliver faster updates, fewer errors, and zero third-party lag.

Tax holidays, reduced rates, sourcing rules, exemptions — we apply the right taxability rules automatically.

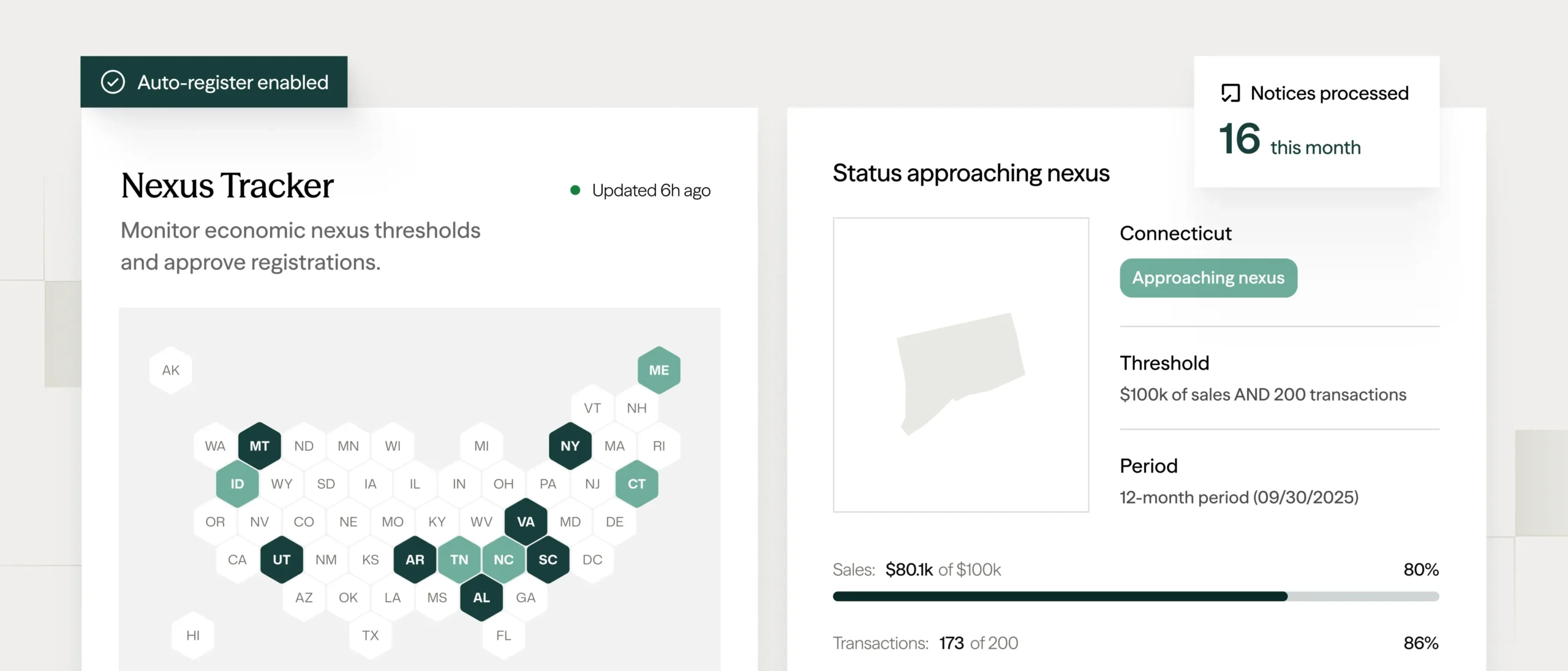

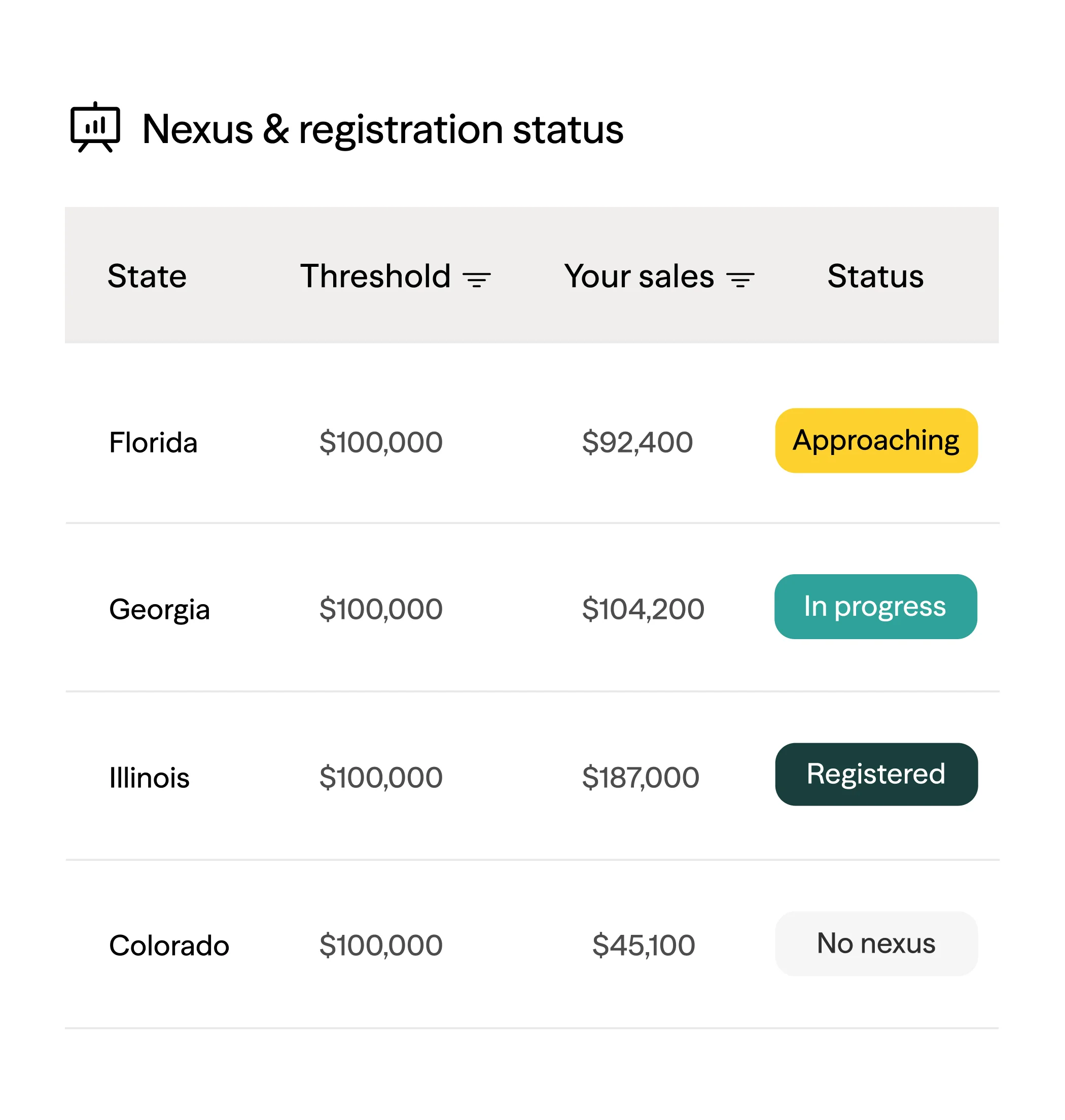

Proactive nexus monitoring & registration.

We monitor your sales across every channel in real time. We tell you exactly when you need to register — and then we handle the paperwork for you.

We alert you when you hit 80% of a state’s threshold so you can plan ahead.

Hit the threshold? We handle the paperwork, linking, and account setup.

State registrations are included in your all-inclusive annual contract.

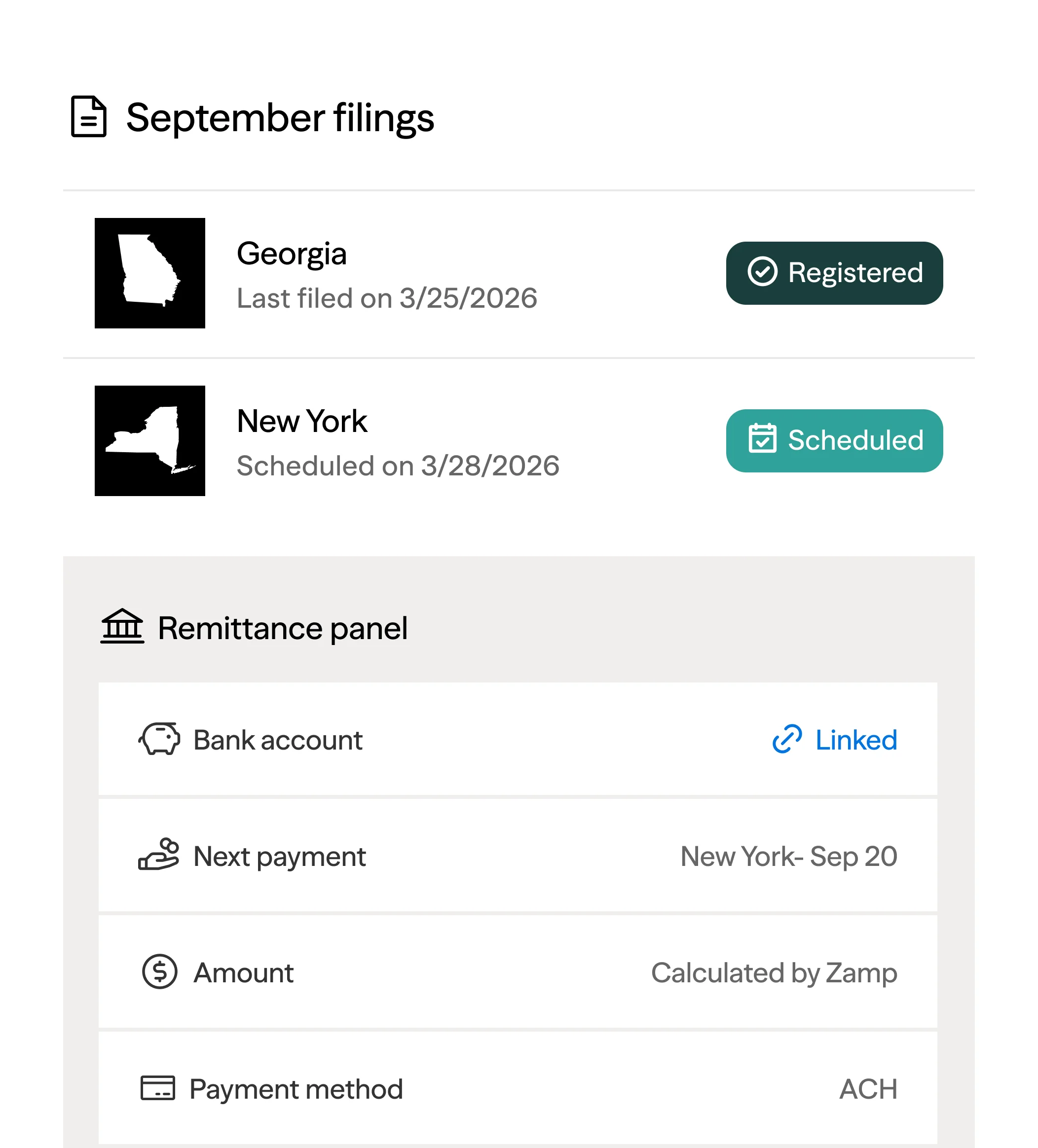

AI-powered filing and remittance on autopilot.

We file your returns, remit the payments, and make sure the state gets paid on time, every time.

We automatically capture "early filing" discounts to lower your bill.

Annual to quarterly? Quarterly to monthly? We adjust your filing frequency automatically.

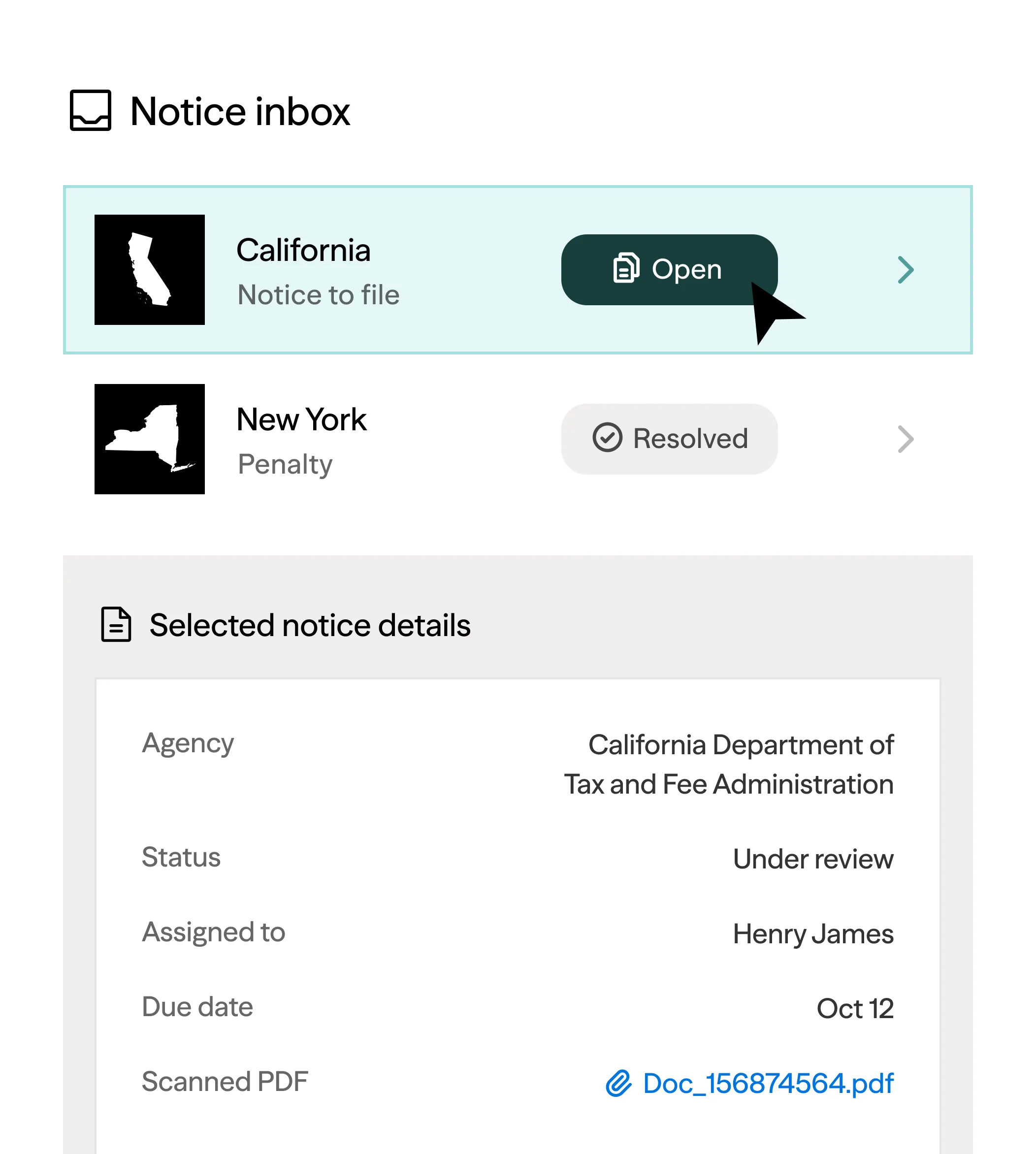

End-to-end notice management.

We monitor state portals daily to catch, interpret, and resolve notices so you never have to decipher them.

We check state portals every day to catch notices immediately.

From simple discrepancies to audit requests, we handle the back-and-forth with the state – streamlined by our AI agents.

We digitize physical mail so you have a complete, searchable history of every notice.

Real tax experts, when you need them.

Our team includes former state auditors and industry veterans. When a complex question comes up — a new SKU, marketplace change, or drop-shipping scenario — you’ll get a fast, clear answer from someone who’s handled it before.

“With Zamp, we’re confidently managing sales tax compliance across 44 states and counting.”

Integrations built for where you sell.

Connect to leading ERP, billing, and e-commerce platforms — and support custom tech stacks via our API.

Everything you need for U.S. and Canadian sales tax — in one place.

FAQs.

Still have questions? Call us at 1-866-438-9267 or email us at support@zamp.com.

Absolutely. Your team retains full control to configure custom product rules, manage exemptions, or override determinations to align with your specific tax strategy.

Yes. Our engine supports non-percentage based fees, such as the Colorado Retail Delivery Fee, applying the correct line item automatically based on the trigger event.

We handle the full complexity of decentralized systems. Zamp automatically identifies and files directly with local agencies, including Louisiana parishes and Colorado home-rule cities.

We automate tax credit recovery. Zamp ingests refunds and chargebacks as credit memos, automatically applying them against your liability so you never overpay the state.

We ensure tax data matches your General Ledger to the penny. Zamp provides detailed reconciliation reports that align collected vs. remitted tax.

Our team analyzes the notice, drafts the response, and communicates directly with the jurisdiction to manage the resolution until the case is closed. Our team proactively closes out notices.

Zamp prepares every return using a dual-check system. While we execute the filing, you retain full governance to review and approve returns in the dashboard before they are submitted.

To ensure speed and transparency. You retain legal ownership of your mail to avoid “black hole” delays. You receive the alert instantly, then simply forward it to us for immediate resolution.