It’s almost the start of the year’s busiest shopping season — Black Friday and Cyber Monday (BFCM). As an online seller or store owner, you’re likely getting ready to release your list of deals and promotions to customers en masse. But one thing you can’t forget as you prepare for the upcoming holiday season is the state sales tax implications that come with selling more goods, items, and services.

Luckily, our team has put together an ultimate guide on sales tax and how to prepare for BFCM 2024. We went in-depth, conducting a survey of 1,000 respondents in the e-commerce industry to see just how ready they are for the upcoming holiday season. We’ll dive more into that and the following:

- What BFCM is

- Whether your business is truly ready for sales tax obligations this holiday season

- Tips on how to prepare for the busiest shopping season this year

Let’s dive in.

What Is BFCM?

While many of us are familiar with Black Friday and Cyber Monday, they are actually two completely separate shopping events targeting different types of sales and customers.

Black Friday is generally seen as the kick-off to holiday season shopping for brick-and-mortar stores and online stores and sales. This shopping day occurs the Friday after Thanksgiving, with Cyber Monday following the Monday after. As its name suggests, Cyber Monday tends to be geared more toward online stores and platforms like Amazon, Etsy, and Shopify.

According to Adobe research, last year’s holiday season generated more than $221.1 billion, with revenue up more than 4% yearly. In addition, Shopify released a report highlighting that merchants using its platform reached a record $9.3 million in sales over the BFCM weekend, a 24% increase from 2022.

All this goes to show that the holiday season generally brings in record-breaking revenue for shops and platforms alike. So whether you own a shop on a platform or a brick-and-mortar store, being prepared to bring in significant revenue is vital for your business’s finances. This includes keeping a touch point on state sales tax laws and nexus thresholds.

Are You Ready for Black Friday 2024?

While you may be gearing up with hiring and inventory for BFCM, there’s one thing just as crucial to prepare for — sales tax. The upcoming holiday season likely means you’ll sell more across various platforms. You may send products to new states where you’ve never sold or even more to states with a solid customer base. What this all equates to is that you may hit nexus thresholds you aren’t aware of.

Understanding sales tax nexus thresholds comes down to the idea of economic presence, which is how much of a connection a business has with a state that makes it subject to sales tax. Most states look at economic factors like how much money a company makes or how many transactions it does in a state.

Zamp Tip

The majority of states have a 200 transaction or $100,000 in sales limit for triggering nexus. For businesses, keeping track of these thresholds and knowing when they need to start collecting sales tax in a new state is vital to staying compliant and avoiding penalties or fines.

BFCM Survey

Our team conducted an in-house survey of 1,000 respondents in the e-commerce industry to determine whether companies are ready for the upcoming BFCM season and handling state sales tax requirements. See more of what we uncovered in the sections below.

Our Survey Respondents

Out of the 1,000 respondents we surveyed, 70.96% work in companies with 250 employees or less. Most of the survey respondents who participated worked in various departments, with the most popular being as a founder or CEO of a company, operations, customer support, and revenue (marketing or sales).

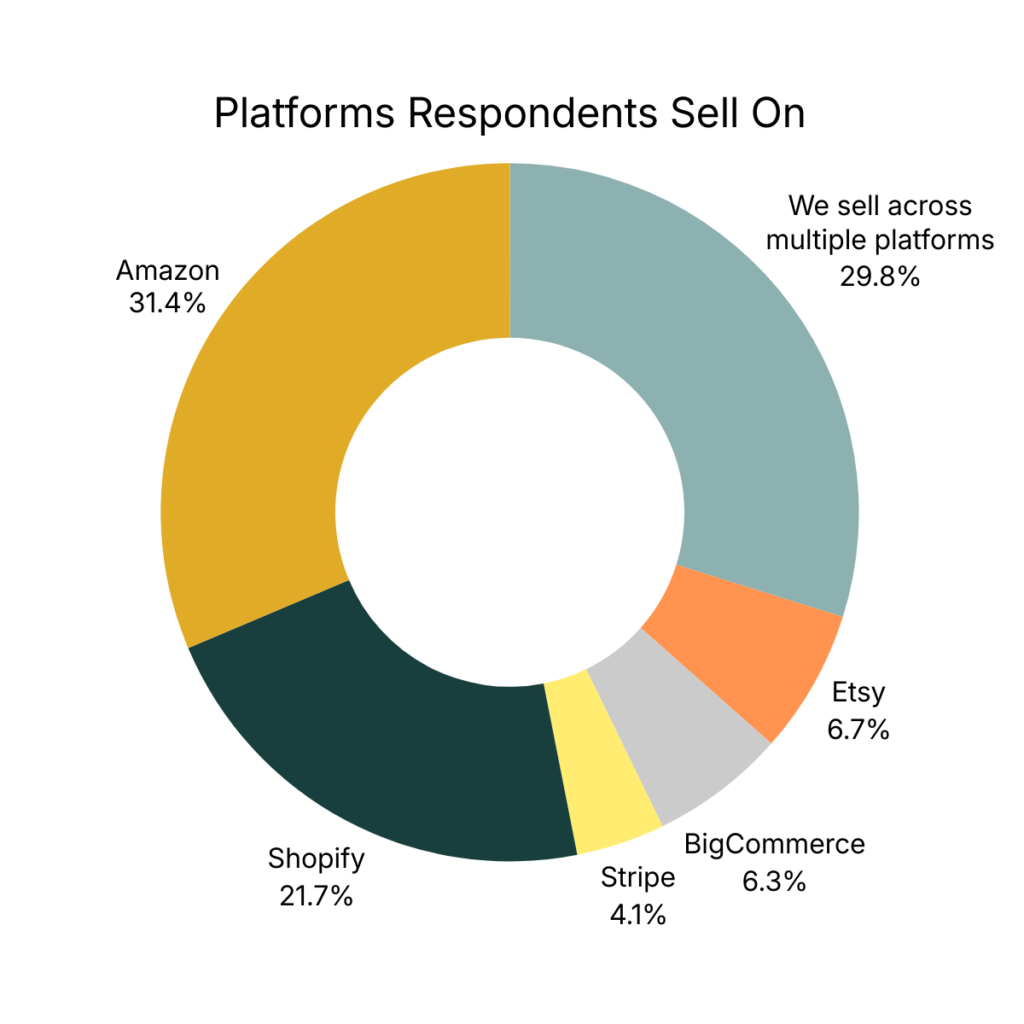

Those who participated sell on various platforms, including Amazon and Shopify. Here’s a breakdown.

In addition, 71% of the 1,000 respondents reported that they use either sales tax software or personnel to help with calculations and nexus tracking. Over 40% stated that they use a combination of both to ensure they are compliant where they do business.

Our Survey Findings on BFCM 2024

Our in-house survey focused on whether companies are ready for the upcoming Black Friday and Cyber Monday shopping season regarding sales tax compliance.

Reflecting on previous years, 92% of the 1,000 respondents reported that their businesses handled sales tax-related issues during BFCM adequately or very well. This compares well to the question we asked on whether companies are confident in their overall readiness for BFCM 2024, where 82.29% of respondents stated they were somewhat confident or very confident for the upcoming season.

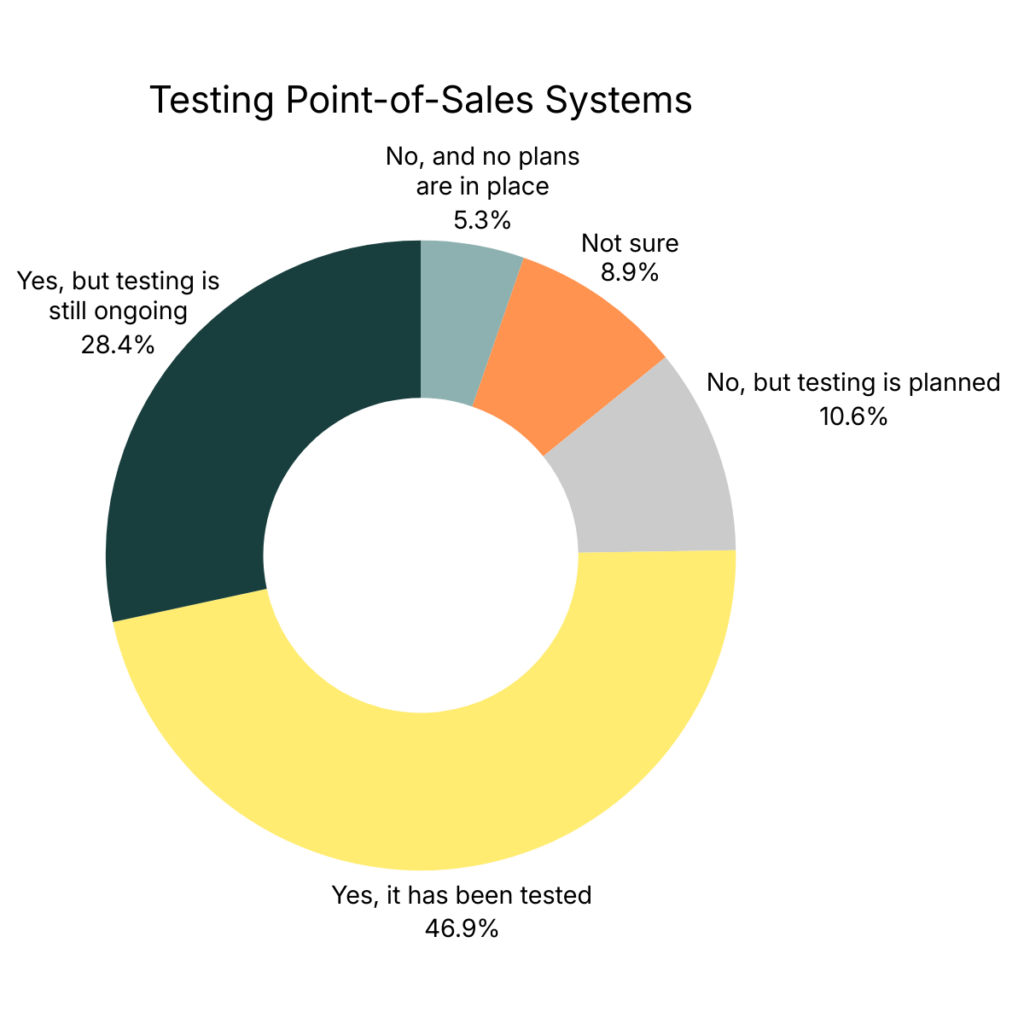

Respondents also reported the following when asked whether their point-of-sale system has been tested for accuracy in tax calculations and handling increased transaction volumes:

BFCM Sales Tax Laws and Requirements

Most e-commerce companies have some tracking in place for where and when they are required to pay state sales tax. But what happens when you hit new nexus thresholds during the busiest time of the year?

Our study found that 76% of those surveyed said they were prepared for the sales tax filing requirements and deadlines after BFCM, while 24% stated they weren’t prepared.

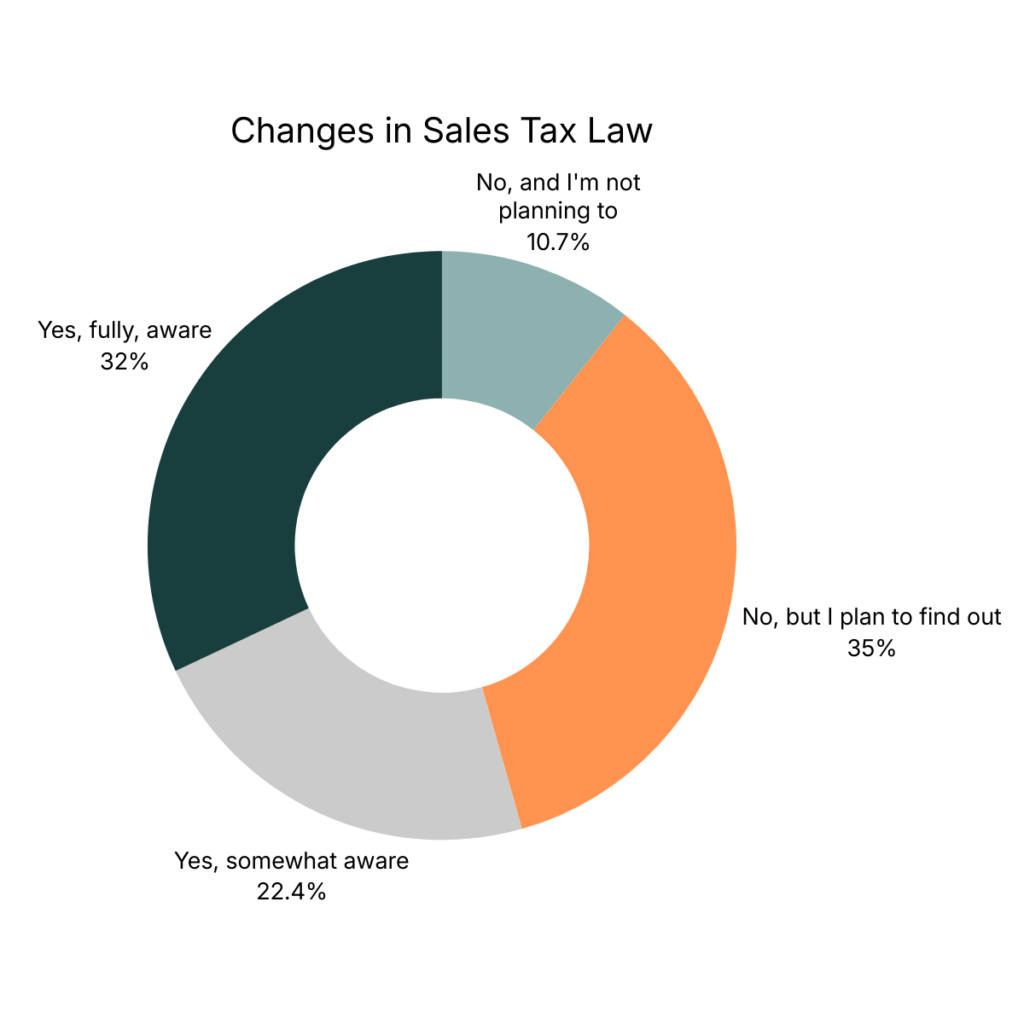

Additionally, we found that over half (68%) of those surveyed in our study are not fully aware of tax laws that could affect their business in the upcoming holiday season. Here’s how that breaks down:

BFCM Sales Tax Concerns and Preparedness

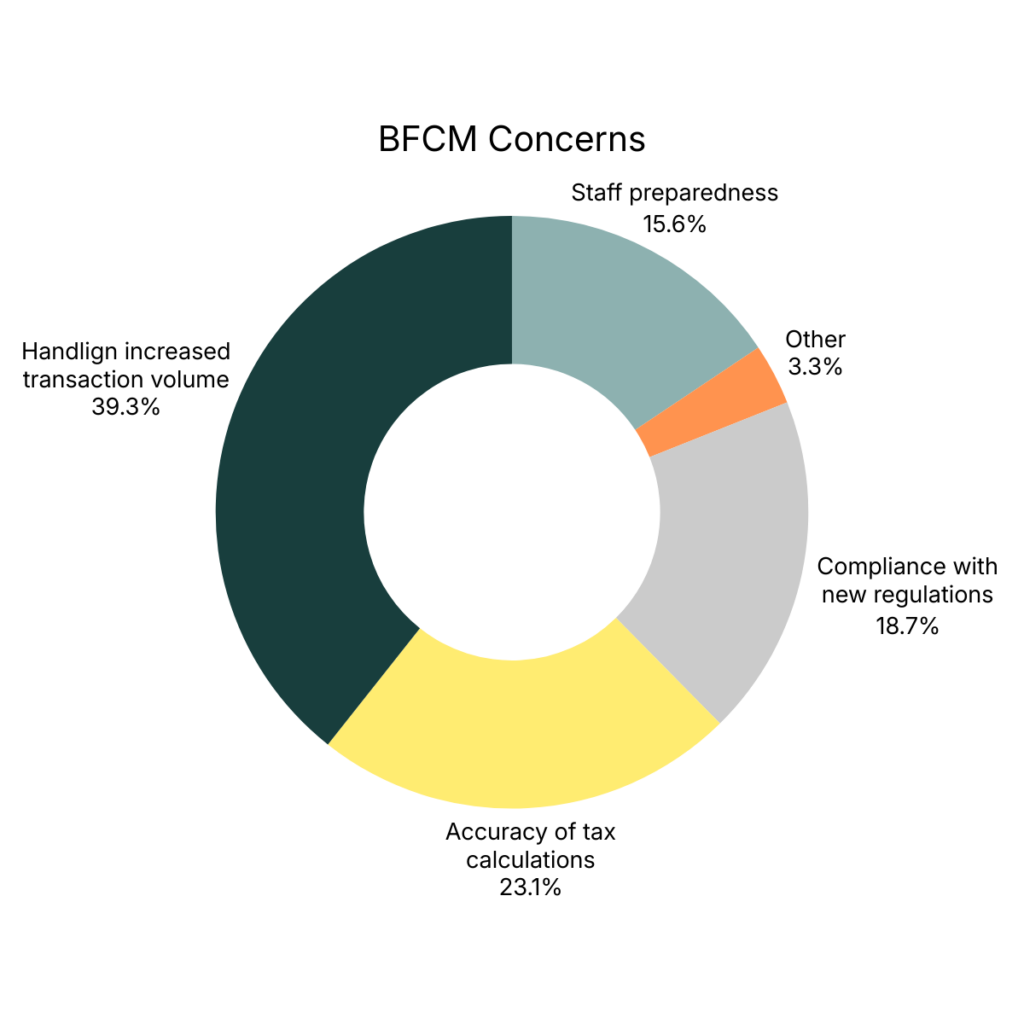

There are many things to be concerned about when it comes to preparing for Black Friday. And that’s why we asked our 1,000 survey respondents from the e-commerce industry what their main concerns were regarding sales tax and BFCM preparation.

Over 39% of those surveyed said they were concerned about handling an increased transaction volume, along with 23% who were worried about the accuracy of sales tax calculations. Let’s take a closer look at these concerns:

With the upcoming holiday season being the biggest shopping time of the year, it’s no wonder e-commerce companies are concerned with sales tax calculations and new regulations.

One of the biggest findings in our survey was that over 47% of respondents stated that they are going to be working with external consultants or professionals to ensure sales tax compliance for BFCM. This is despite the fact that 40% of those surveyed already have in-house personnel and software to track sales tax compliance and nexus for them.

If you’re looking for an automated sales tax solution and an in-house team with a combined 200 years of sales tax, book a call with Zamp. We’re a full sales tax compliance service that checks all the boxes — nexus tracking, registrations, roof-top accurate calculations, product taxability research, mapping, filing, and reporting. See why our customers trust us to handle all their sales tax needs.

Preparing Your Business for Black Friday 2024

With the holiday season just around the corner, there are several things you can do to prepare your business for Black Friday and Cyber Monday. The most important from a sales tax perspective is:

- Ensuring you have tracking set up for sales

- Knowing the nexus thresholds

- Making sure you file state sales tax returns

1) Ensure Tracking Is Set Up for Sales

As discussed above, economic nexus centers around how much money you make from sales and/or transaction volume in a particular state. Companies and e-commerce merchants selling across multiple platforms need to have a clear nexus or sales tracking setup to know how much they are selling across channels and where.

Any seller or business owner needs to know that nexus isn’t broken up by platform or selling channel; it’s all tracked at the state level. This means that no matter what type of good, product, or service you sell, it all counts toward nexus activity in a state.

Having an automated sales tax solution like Zamp ensures a hassle-free sales tax experience year-round. Our automation handles everything from getting started to nexus monitoring and adapting to new tax rules. You can focus on your business while we handle sales tax compliance.

2) Knowing Nexus Thresholds Where You Operate

Making sure your business has a good tracking setup is just the first step. You also need to ensure you understand the thresholds in the states you do business in.

If you’re a store owner who only sells in a brick-and-mortar environment, you likely only have to worry about a limited number of states. On the other hand, e-commerce businesses can be complicated as you’re essentially responsible for managing sales tax nexus across the entire US.

While the shipping destination determines which state has jurisdiction over your sales tax obligations, it’s essential to know that you only need to collect in states where you’ve triggered economic nexus or have a physical presence, referred to as physical nexus.

We researched the economic nexus requirements for each state. You can find out more in the table below.

| State | Economic Nexus Threshold | Source |

|---|---|---|

| Alabama | Retail sales of more than $250,000 made directly by the seller during the previous calendar year. | Alabama Department of Revenue |

| Alaska | While Alaska has no statewide sales tax, some municipalities have a local sales tax. In those cases, the nexus threshold is $100,000 in gross annual sales or 200 annual transactions. | Alaska Remote Sellers Sales Tax Commission |

| Arizona | Gross sales of $100,000 or more in the previous or current calendar year. | Arizona Department of Revenue |

| Arkansas | Taxable sales of more than $100,000 or more than 200 transactions during the previous or current calendar year. | Arkansas Department of Finance and Administration |

| California | Sales of tangible personal property exceed $500,000 during the preceding or current calendar year. | California Department of Tax and Fee Administration |

| Colorado | More than $100,000 in retail sales in the preceding or current calendar year. | Colorado Department of Revenue |

| Connecticut | Retail sales of at least $100,000 and 200 transactions during a 12-month period. | Connecticut Department of Revenue Services (Conn. Gen. Stat. sec. 12-407(a)(15)(v) |

| Florida | Taxable retail sales of tangible personal property exceed $100,000 over the previous calendar year. | Florida Department of Revenue |

| Georgia | Gross revenue from retail sales of tangible personal property exceeds $100,000, or the number of retail sales of tangible personal property is 200 or more in the previous or current calendar year. | Georgia Department of Revenue |

| Hawaii | Gross proceeds of $100,000 or more, or 200 or more separate transactions in the preceding or current calendar year. | Hawaii Department of Taxation |

| Idaho | Sales exceed $100,000 in the previous or current calendar year. | Idaho State Tax Commission |

| Illinois | Gross receipts from sales of tangible personal property of $100,000 or more, or the seller makes 200 or more separate transactions during the previous 12-month period. | Illinois Revenue |

| Indiana | Gross revenue exceeds $100,000 in the previous or current calendar year. | Indiana Department of Revenue |

| Iowa | Gross revenue exceeded $100,000 in the previous or current calendar year. | Iowa Department of Revenue |

| Kansas | Gross sales exceeded $100,000 in the previous or current calendar year. | Kansas Department of Revenue |

| Kentucky | Gross receipts from sales exceed $100,000, or the seller makes 200 or more separate transactions in the previous or current calendar year. | Kentucky Department of Revenue |

| Louisiana | Gross revenue from sales exceeds $100,000 in the previous or current calendar year. | Louisiana Department of Revenue (La. Revenue and Taxation sec. 47:30(4)(m)(i) |

| Maine | Total gross sales of tangible personal property or taxable services in the previous or current year exceed $100,000. | Maine Revenue Services |

| Maryland | Gross revenue from sales exceeds $100,000, or the number of transactions is 200 or more during the previous or current calendar year. | Comptroller of Maryland |

| Massachusetts | Sales exceed $100,000 in the previous or current taxable year. | Massachusetts Department of Revenue |

| Michigan | Gross sales (taxable and nontaxable) in the prior year exceed $100,000, or the number of transactions exceeds 200. | Michigan Department of Treasury |

| Minnesota | Retail sales exceed $100,000, or the seller made 200 or more retail sales in the previous 12 months. | Minnesota Department of Revenue |

| Mississippi | Sales of more than $250,000 in the previous 12 months. | Mississippi Department of Revenue |

| Missouri | Gross receipts from taxable sales of tangible personal property exceed $100,000 annually. | Missouri Department of Revenue |

| Nebraska | Retail sales of more than $100,000, or the number of separate transactions is 200 or more during the previous or current calendar year. | Nebraska Department of Revenue |

| Nevada | Retail sales of more than $100,000, or the number of separate retail transactions is 200 or more in the previous or current calendar year. | Nevada Department of Taxation |

| New Jersey | Gross revenue from sales of tangible personal property, specified digital products, or taxable services exceeds $100,000, or the number of separate transactions is 200 or more in the previous or current calendar year. | New Jersey Division of Taxation |

| New Mexico | Taxable gross receipts of at least $100,000 in the previous calendar year. | New Mexico Taxation and Revenue Department |

| New York | Gross receipts from sales of tangible personal property exceed $500,000, and the seller made more than 100 sales of tangible personal property in the previous four sales tax quarters. | New York Department of Taxation and Finance |

| North Carolina | Gross sales exceed $100,000 in the previous or current calendar year. | North Carolina Department of Revenue |

| North Dakota | Taxable sales exceed $100,000 in the previous or current calendar year. | North Dakota Office of State Tax Commissioner |

| Ohio | Gross receipts exceed $100,000, or the seller makes 200 or more separate transactions in the previous or current calendar year. | Ohio Department of Taxation |

| Oklahoma | Taxable merchandise sales exceed $100,000 in the previous or current calendar year. | Oklahoma Tax Commission |

| Pennsylvania | Gross sales exceeding $100,000 in the previous calendar year. | Pennsylvania Department of Revenue |

| Rhode Island | Gross revenue from sales of $100,000 or more, or the number of separate transactions is 200 or more in the previous calendar year. | Rhode Island Division of Taxation |

| South Carolina | Gross revenue from sales of tangible personal property, products transferred electronically, and services delivered into the state exceed $100,000 in the previous or current calendar year. | South Carolina Department of Revenue |

| South Dakota | Gross revenue from sales exceeds $100,000 in the previous or current calendar year. | South Dakota Department of Revenue |

| Tennessee | Retail sales of $100,000 or more in the previous 12-month period. | Tennessee Department of Revenue |

| Texas | Total revenue of $500,000 or more during the preceding 12 calendar months. | Texas Comptroller |

| Utah | Gross revenue from sales of tangible personal property, products transferred electronically, or services exceeds $100,000, or the seller makes 200 or more separate transactions in the previous or the current calendar year. | Utah State Tax Commission |

| Vermont | A minimum of $100,000 in sales or at least 200 individual sales transactions during the preceding 12-month period. | Vermont Department of Taxes |

| Virginia | Annual gross retail sales exceed $100,000, or the seller makes 200 or more sales transactions in the previous or current calendar year. | Virginia Tax |

| Washington | More than $100,000 in cumulative gross receipts in the current or prior year. | Washington Department of Revenue |

| Washington DC | Gross receipts of more than $100,000, or the number of separate retail transactions is 200 or more in the previous or current calendar year. | Washington DC Office of Tax and Revenue |

| West Virginia | Gross sales of $100,000 or more, or the number of separate transactions for goods or services is 200 or more in the preceding or current calendar year. | West Virginia Tax Division |

| Wisconsin | Gross sales exceed $100,000 in the previous or current calendar year. | Wisconsin Department of Revenue |

| Wyoming | Gross revenue from the sale of tangible personal property, admissions, or services delivered exceeds $100,000 in the preceding or current calendar year. | Wyoming Department of Revenue |

3) Make Sure You File State Sales Tax

If you hit new nexus thresholds during BFCM or any other time of year, you’ll need to register in each state you hit nexus in to file a sales tax return. You may have to file monthly, quarterly, or bi-annually, depending on how much you sell each year.

If you don’t register or file taxes in the states you owe, you’ll face penalties or fines. These can sometimes be seen as a minor inconvenience but can end up costing you down the road. Fines can sometimes reach up to 25% of the unpaid tax.

With so much that can go wrong, we recommend contacting our sales tax experts at Zamp. They can help you set up everything correctly and ensure you register and file in states where needed. Book a call today.

Conclusion

While sales tax should always be a concern, it can be extremely problematic during the holiday season as you sell more products and services than usual. Ensuring that you track sales tax data and nexus thresholds across platforms and register and file in states where needed is vital for any business to remain compliant. Otherwise, you may be hit with hefty penalties or fines.

Zamp is the first fully managed sales tax solution in the market, which allows you to outsource your sales tax compliance from start to finish. We offer hands-off onboarding with our experienced and dedicated onboarding representatives and a complete service that checks all the boxes, from nexus tracking to registrations, reporting, and filing. Book a call and see how we can help!

Get Help for Your Company

30-minute call

sales tax expert

off your plate